The Geopolitics of Israel’s Offshore Gas Reserves

By David Wurmser

The Finance Ministry expects gas production from the Tamar natural gas field to contribute 0.8% to GDP for 2013 – – Photo: Albatross Aerial Perspective/AP

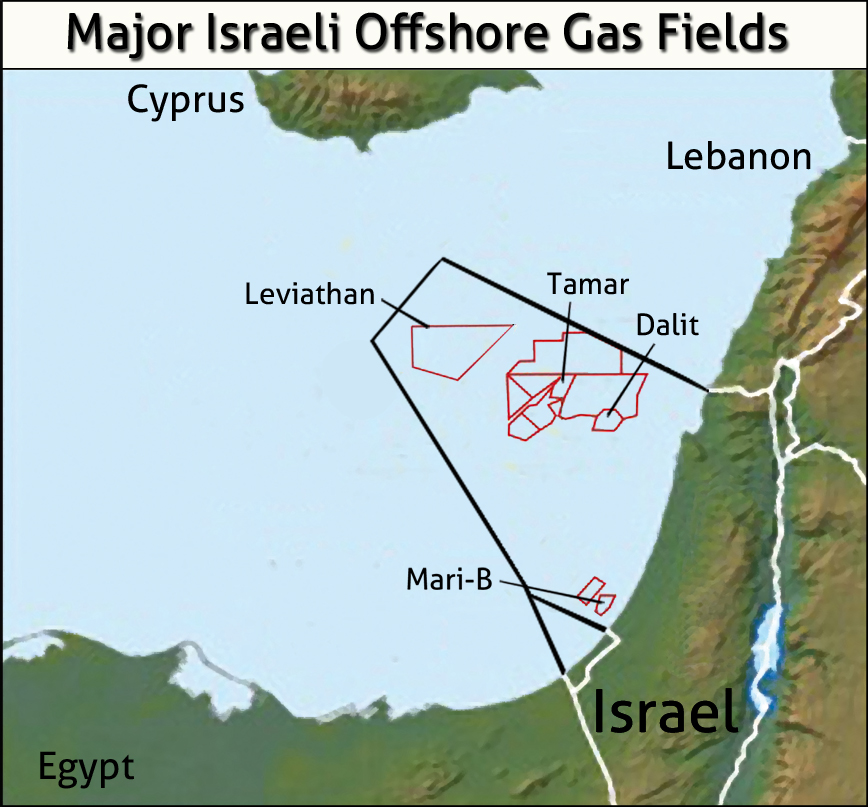

- On January 17, 2009, Israel’s economy and even its strategic stature changed when a team led by the Texan firm Noble Energy discovered gas in the Tamar field in the eastern Mediterranean, which is estimated to contain 9.7 trillion cubic feet (TCF) of natural gas. The Tamar well-heads which contain methane gas are rated at a high level of purity, with an energy value of production per well-head over four-fold higher than Saudi oil well-heads. Two years later, the same team drilling a few dozen kilometers further west discovered a monstrous gas field, appropriately called Leviathan, which is now estimated to contain 18 TCF and could begin supplying gas in 2016.

- Tamar was only the beginning. The amount of gas subsequently discovered offshore now dwarfs any feasible, projected Israeli demand for at least half a century. The Tamar field alone represents two decades of consumption. As such, Israel will become a net exporter of gas. The Israeli gas discoveries in the eastern Mediterranean are only part of new gas fields in what is called the Levant Basin, which includes the maritime areas of Israel, Cyprus, Lebanon, and even parts of Syria’s waters. The Levant Basin could hold 125 TCF – about one-third of Russia’s gas reserves.

- The most likely short-term destination for Israel’s natural gas is Jordan. Connecting Israel’s emerging gas grid to Jordan is a relatively inexpensive and simple endeavor. Yet Israel will almost certainly have much larger amounts to export.

- Given its geographic proximity, Europe would seem to be the natural export market for Israeli gas. Moreover, Europe is facing a major gas supply crisis because of the spread of instability in Algeria and the rest of North Africa. Yet Asia may emerge as Israel’s preferred export destination. The Australian firm, Woodside, which acquired about a third of the rights to the Leviathan field, is oriented toward marketing gas in Asia, and envisions building a liquefaction plant to service that trade.

- Israel’s recent experience with Egypt, where half of its natural gas supply was permanently severed following the collapse of the Mubarak regime, suggests that Israel will view with apprehension any scheme to anchor its critical infrastructure in countries beyond its own borders, such as Jordan, Cyprus, or Turkey. Thus, it is likely that ultimately the gas will be liquefied on Israeli territory and exported directly via sea to the consuming market.

- Israeli officials view a cross-Israel natural gas pipeline connecting the Mediterranean and Red Seas as an alternative to the Suez Canal. But an export structure operating directly from Eilat to markets in Asia would face a rising strategic problem: Iran’s increasing naval presence in the Red Sea. This will require Israel to establish and expand a Red Sea fleet as well as a significant expansion in the size and capability of its Mediterranean fleet.

On January 17, 2009, Israel’s economy and even its strategic stature changed. A team led by the Texan firm Noble Energy Inc., drilled under 5,600 feet (1,700 meters) of water and 16,000 feet (5,600 meters) of rock and salt off Israel’s shores in the Matan license to explore a prospect called Tamar. On that day, they struck and flared methane, discovering a field which now is estimated to contain a probable 275 billion cubic meters (9.7 trillion cubic feet, or TCF) of natural gas. To compare the size of the field to consumption measures, the field represents over half of what the European Union’s 27 (EU-27) nations consume annually, which in 2010 peaked at about 522 BCM before declining in 2011 and 2012, of which now about 463 BCM is imported per annum). Moreover, the Tamar well-heads which contain methane gas are rated at a high level of purity, with an energy value of production per well-head over four-fold higher than Saudi oil well-heads.

While the economic and resource effects of this and subsequent finds are becoming clearer by the day, the complex geo-strategic context and significant implications of the finds remain largely under-examined. And that complexity and impact will dramatically increase if – as we will learn late in 2013 – oil is discovered under the gas or if the touted new technologies to extract Israeli shale oil prove real.

What Was Found and How to Understand It

Discoveries Off-Shore of Israel and Cyprus

Almost two years after the large Tamar field was found, the same team drilling a few dozen kilometers further west announced yet another discovery, this time of a monstrous gas field, coincidentally but still appropriately called Leviathan, straddling the Rachel and Amit licenses. Leviathan alone is now estimated to contain 18 TCF, namely about as much gas as Europe consumes annually. Ever since, there have been several other finds of smaller, but nevertheless substantial fields, such as the Karish (Shark) field, which contains possibly about half as much gas (3 TCF) as Tamar, and the Dophin 1 field in the Hanna license announced in November 2011, which may add another TCF to Israel’s tally – a small amount, but nevertheless still enough alone to fuel Israel’s domestic gas needs for several years. At least another TCF appears to have been found as well in the Tanin (Crocodile) field in the Alon license. There are also several other unexamined natural prospects in various stages of exploration.

In neighboring Cyprus, another field (Aphrodite) comparable to the Tamar find was discovered – also by Noble Energy. It abuts and even slightly spills into Israel’s waters into a series of prospects known as the “Pelagic licenses.” And the growing Israeli-Cypriot relationship, as well as the overlap of some of the consortia involved in exploration and production activities, suggests that the two nation’s hydrocarbon assets and activities can reasonably be seen as a potentially integrated whole.

In short, Israel and its Greek island neighbor now sit atop of at least 35-40 billion cubic meters of gas – roughly two-years’ worth of European consumption – and still have broad areas of exploration ahead of them. Indeed, Israel’s Oil Commission at the Ministry of Energy and Water Resources has closed further offshore licensing until the 40 current exploration licenses, which cover 65 percent of Israel’s economic waters, are completed. Israel has not granted any new licenses since March 2010. Moreover, Cyprus’ waters remain largely unexplored. In fact, only one block (block 12) has been systematically examined. Only since the end of 2012 were tenders awarded for exploration in several more blocks, with international majors, such as Total, leading the pack.

What May Still Lie Beneath

In 2010, the United States Geological Survey (USGS) issued a resource estimate report. Based on information now likely outdated since it was issued even before the Leviathan discovery, it estimated even then that the Levant basin could potentially hold as much 125 TCF of recoverable gas – an amount representing about one-third of Russia’s known reserves. The Levant basin is a geological delineation that includes the maritime areas of Israel, Cyprus, Lebanon and even parts of Syria’s waters. Egypt’s natural gas (which includes several dozen TCFs of natural gas) is considered a different basin, as are any potential discoveries in Greek waters or areas north of Cyprus. Moreover, in 2011 a team of geologists from MIT examined data from the Levant basin and concluded that Israel “can expect at least 6 more ‘Leviathans’ in its territorial waters” (at the time Leviathan was thought to hold 16 TCF; today it is estimated to hold 18 TCF).1 If such estimates pan out, Israel alone could potentially posses about a third as much as Russia’s natural gas reserves.

But there is a caveat. While still important, geological reports such as the ones issued by USGS and MIT are primarily indications of the basin’s considerable potential beyond discoveries thus far announced. They are scientific guesses based not on discovered, nor even reliably likely to be discovered, amounts, and may not even be based on the latest and most sophisticated data from 3-D seismic studies and actual exploratory drilling, all of which is superior information which exploration and production (E&P) companies themselves gather and hold. As such, E&P companies do take notice when such reports are issued – it grabs attention and warrants dedicating resources to examine more thoroughly – but actual investment and acquisition decisions are made on the basis of known discoveries and data, not USGS or MIT estimates.

Exploration remains the domain of people with a gambling soul, not those averse to risk, because even the most promising estimated prospect can turn out to be a dry hole, and exploration estimates based even on 3-D seismic studies which are set above 30 percent likelihood are considered very high. Indeed, the story of two prospective fields in Israel shows just how risky it is to bet even on high likelihoods in gas. The Ishai license of the “Pelagic” group turned out to lack substantial gas even though 3-D seismic studies showed much promise and it abutted the large Aphrodite field across the EEZ line in Cyprus. The Myra and Sarah licenses were also at first thought to hold as much as 6 TCF on the basis of 3-D seismic studies. In short, to take concrete action – whether it is a firm making an investment decision or a nation making a strategic decision – based on these studies is high-risk.

As such, while not belittling the potential of further finds, not only of gas, but oil as well – many of which can be cataclysmic, game-changing events for Israel (and could potentially propel Israel into becoming a hydrocarbon-producing super-power) – current analyses of the economic, strategic and political impact of gas in the basin should still be anchored to announced discoveries and ongoing exploration activities and data collected by companies, and not on governmental or non-oil industry estimates.

History and Background

Up until the middle of the last decade, British Gas owned most of the licenses in Israel. But in 2005 and 2006, it sold its rights and swore off ever returning to Israel, despite the fact that there were geological indications of hydrocarbons deep below.2 It sold the Matan license in 2005, which then became known as the Tamar Reserve, to Avner Oil and Gas for only $1. Avner Oil and Gas eventually transferred part of its stakes to Delek Energy (both Avner and Delek are part of the larger Delek conglomerate under Yitzhak Tshuva) and sold more to Noble Energy, Inc. in 2006.3

Gas had already been found a decade earlier than the Tamar discovery of 2009 in smaller offshore fields, but the amount of gas in those wells represented a momentary – and even then partial – relief to the complete dependence Israel faced in its energy sector. The main field – known as Mari-B – contained about 1 TCF of gas (about as much as the Dolphin 1 field announced in late 2011). Despite its limited size, it did, however, play an important role in helping Israel transit from exclusively using heavy fuel oils and coal for electricity production to become a more clean-burning and gas-reliant nation in terms of electricity production. Mari-B, which was the first source for Israel’s gas-fired power plants (starting in 2004), was soon joined by the import of Egyptian gas, which had been planned first, but was delayed in arriving by several years.

By the end of the decade (2009-2010), gas supply from Egypt accounted for about half of Israel’s gas consumption (40 percent), and gas from Mari-B supplied roughly the other half (60 percent).4 The two together transformed Israel into a country relying on gas for about 40-45 percent of its total electricity production by 2010, up from none only half a decade earlier. Israel is now on its way to become one of the most gas-reliant nations for electricity production in the industrialized world, with estimates ranging well over 60 percent reliance within a few years.

This trend toward reliance on gas predated the discovery of Tamar, largely because of the assumption that gas from Egypt – which sold for less than 25 percent of the price of the equivalent heavy fuel oil used for energy production – would greatly relieve Israel’s eternally tenuous and expensive quest for such fuel, and would provide a long-term solution for Israel’s energy needs. Even then, it was recognized that the Mari-B field, which only contained about 1 TCF, could supply Israel until 2013-14 – or a bit over half a decade – before it would be fully depleted.

As such, before the discovery of Tamar, Israel had already been moving to cheaper and cleaner energy production with the transition to natural gas, but it was not really gaining energy independence in the medium- and long-run. Israel was slated to become fully dependent on Egyptian gas by 2014 to fuel about half of its electricity production.

Gas as Peace

While aware of the danger associated with such dependence on its neighbor, Israel hoped that this dependence could be rendered safe by anchoring it to the vital national interests of the Egyptian economy and to the personal interests of its elites. By helping the fortunes of Egypt’s business and ruling elite and providing a source of revenue to the Egyptian state – thus locking it in to a fiscal dependence – the gas trade could bring meaningful substance to the idea of “normalization” – the idea that daily interactions between the people and economies of Israel and Egypt would transform the peace treaty signed in 1979 from a formal but detached treaty between governments into a daily reality, co-dependence and a source of familiarity among the two nations’ peoples. Indeed, the Egyptian-Israeli natural gas trade was the culminating, and only now understood to be final, act in the attempt to solidify Egyptian-Israeli relations (and financially shore up the Egyptian government and its elites) through trade.

It was in this context that the discovery of gas off of Gaza should also be understood. In 2000, gas was found offshore in the Gaza Marine prospect. The field was roughly comparable to Mari-B, which lies offshore from Ashdod. The Gaza Marine field held the potential for helping the Gazan economy develop, fund the Palestinian Authority, and tie Israel’s and Gaza’s economy together, and had the potential of becoming a supporting column in the edifice of peace. The discovery, and hopes for its expeditious development, thus paralleled the attempt to lock the Egyptian-oriented Palestinian pan-Arab nationalist leadership into a peace process through economic interdependence and revenue incentives to elites.

At the time, the British Gas Group (BG) owned the Gaza Marine field (as it still does) as well as all the known Israeli fields (all of which it sold). To help the development of the Palestinian economy – which was seen as key by Israeli and American leaders to politically moderating the Palestinian population and solidifying peace – and lay to rest any potential arguments in the future over the resource, Israel carved from within the demarcation of its proposed Exclusive Economic Zone (EEZ) between itself and Gaza an indentation rather than run the demarcation line straight from the coast as is done in every other EEZ demarcation across the globe. Israel agreed to allow the line to be indented to Israel’s disadvantage so that the entirety of Gaza Marine will be included in the Palestinian Authority area. The gas, which was to be used both inside Gaza for electricity production and exported to Israel, was to help the Palestinian Authority fund itself, have resources to build up its stature among Palestinians, and by stimulating development, to encourage political stability and moderation.

In 2013, talks reportedly resumed between Israel and the British Gas Group (which owns 60 percent) and its partners: Consolidated Contractors Company (CCC), owned by Lebanon’s Houri family, which owns 30 percent, and the Palestinian Investment Fund (PIF), which owns 10 percent), to develop the reservoir for the Palestinian population in the West Bank and Gaza.5 Apparently, the talks centered on having the gas service the Palestinian Authority areas, which currently have only one 240-megawatt plant powered by diesel, though there are plans to build four natural gas power stations in the West Bank.

In the past, Israel had discussed developing the Gaza Marine reservoir to supply Israel as it entered its own natural gas shortage following the cessation of gas deliveries from Egypt. Going back further – and the most probable scenario if it ever comes to pass (which is unlikely) – BG has unsuccessfully tried to sell gas to the Israel Electric Corporation (IEC). The amount of money the IEC loses annually – since the Palestinian Authority is connected to Israeli power but is not paid by the Palestinians – roughly equals the value of the gas which could be extracted per annum from Gaza Marine. There could be a swap – Israeli electricity for gas – without actual money being exchanged, which would go some way toward addressing Israel’s concern that revenue collected from Gaza Marine gas sales to others would eventually wind up funding Palestinian terrorism against Israel.

Gas Trade from Israel’s Neighbors

These attempts to anchor Israel’s relationships to economic interests became a casualty first of the Palestinian elections of 2006, in which Hamas prevailed and which facilitated Hamas’ assertion of control over Gaza, and then five years later with the Arab Spring (Sunni Awakening), starting in 2011.

Despite hopes for its role in encouraging peace between Israelis and Palestinians, Gaza Marine was never developed. Few really wanted the gas to come to market. Egypt saw it potentially as competition to its own gas agreement with Israel (unless the whole affair would have been transferred under their structure), nor did it genuinely ever pursue policies which would make the Gaza Strip a truly viable economic player independent of Cairo’s continued largesse. Israel by and large feared that absent any controlling mechanism, the revenue from the gas sales accruing to the Palestinians would flow to terrorist entities in Palestinian areas.

Iran – which developed operational control over the most powerful and violent elements of Hamas – opposed the deal, as it did the development of Lebanese gas, since it competed with its own gas. Moreover, Tehran generally pursued a policy of enfeebling the Palestinians in order to exploit their misery for their own strategic purposes. Russia as well was lukewarm to any effort not under their control, and even made efforts to buy Gaza Marine, at first outright and then in hidden fashion through a Norwegian firm. Great Britain blocked both paths to a sale, likely under encouragement from the United States. To this day, British Gas continues to seek a buyer for the moribund Gaza Marine project.

Finally, perhaps portending the difficulties which await Lebanon’s communities as they grapple with their possible natural gas discoveries, the internal divisions among Palestinians and their fractured political community all but guarantee that Gaza Marine will remain stranded under the Mediterranean for quite a while. When Hamas assumed control over Gaza, it insisted that the agreements between the PLO and British Gas were null and void. Hamas claimed that the agreements had been corrupt arrangements between the West and the local elite attempting to enrich itself, and that the intermediary company, CCC, was a Christian entity which could not represent the interests of the Islamic community over their inherited resource. The Palestinians never managed to overcome these profound differences, and the gas remains undeveloped.

Many of the arguments arising in Gaza by 2008-9 began to appear in the public debate in Egypt as the gas trade with Israel commenced. The main line of public criticism of the Mubarak regime on this issue was that it was a corrupt agreement which was designed to enrich the elites and sell out the interests of the Egyptian people to advantage the Jews and the West. Gas shortages in Egypt – which were for a different type of natural gas for cooking rather than power production, and which were the result of poor distribution networks – were also immediately attributed to the gas trade with Israel. The main figure behind the Egypt-Israel gas deal, Hussein Salem, was allegedly receiving enormous kickbacks from the trade, and was strongly associated with Gamal Mubarak, the president’s son. Indeed, since Egypt’s political class opposed not only gas export in general – particularly to Israel – but any element of normal relations between the two countries, the fact that the Egyptian-Israel peace was devoid of interaction beyond formal diplomatic relations made the gas trade stands out. Precisely because it had become a meaningful element of normalization between the two countries, opponents of the Egyptian-Israeli peace agreement saw its termination as a vehicle to gut the treaty.

In late 2009, Egypt’s government was defending the gas trade with Israel. Egypt’s Petroleum Minister, Sameh Fahmi, tried to justify the trade as required under the 1979 agreement, but quickly realized that appeal to the requirements of the peace treaty only intensified opposition – since trying to sabotage normalization with Israel was precisely the point of much of the opposition – and confirmed the trade’s non-economic moorings. In the last days of the Mubarak regime, Fahmi tried to justify selling Egyptian gas to Israel for numerous national economic, legal and strategic reasons, but ultimately suggested the decisive reason is that Egypt is expropriating Israeli wealth by charging Israel more than it charges other buyers.6 In other words, the only reason the Mubarak government could raise at the end for continuing the gas trade with Israel was that it helped relieve Jews of their wealth.

It was not surprising, then, that within weeks of Mubarak’s fall, the Egyptian-Israeli gas trade – upon which Israel had become dependent – was interrupted almost continually throughout 2011, and then came to a formal end by the end of the year, even though Israeli officials to the end dismissed the likelihood of such a termination, citing the fact that the Egyptian state could ill afford to lose such a significant source of hard cash and foreign currency. In the mid-1990s, Israel misjudged how eager the PLO would be to come to an acceptable arrangement to bring Gaza gas on line because its finances depended on it. A few years later, Israel misjudged as well how strongly antipathy toward Israel would also trump the fiscal interests of the Egyptian state.

The discouraging precedents of potential Egyptian and Gazan gas trade with Israel, or lack thereof, suggest the danger of hoping that leveraging Israel’s gas trade with other neighbors could alter the direction of their relations with Israel, whether it be with Amman or Ankara.

This also highlights the importance of the discovery at the Tamar field – which was found just as the Egyptian gas trade entered turbulence before plummeting to zero, and just as the Mari-B field entered its last stages of production. Tamar averted what would have been a major breakdown in Israel’s energy sector. And Tamar, and the finds which have followed, now represent Israeli natural gas independence for the next two decades, just as Israel found itself unable to continue the energy dependence which it had built and upon which it had counted from its neighbors in the anticipated but now fading age of peacemaking.

Economic and Resource Impact

The most immediate and potentially greatest strategic impact of Israel’s new energy reality is the effect it will have on the ultimate foundation of the nation’s long-term strength: its economy. The Tamar find and those following it opened a new chapter which will fundamentally change Israel’s resource circumstances and economy. Israel had labored since its creation under resource scarcity. The gas discoveries now position it to become a significant exporter of energy rather than a scrambling purchaser of it. Moreover, not only will this save Israel tens of billions of dollars in external payments annually to buy its energy, but Israel can now turn the abundance of cheap and relatively clean energy to launch large-scale desalination and leverage its fortune to end another resource scarcity – water. Indeed, Israel may now become a net exporter of water, not only energy, as it frees up the Sea of Galilee to possible export to neighboring Jordan rather than continue to use large amounts of energy in an expensive effort to pump its water to Israeli cities. Ending its resource dependence in its two most critical sectors answers strategic challenges which had placed Israel in a dangerously vulnerable position since birth. At the same time, it will contribute to Israel’s growing strategic confidence.

Economically, Israeli industries will see a dramatic decrease in production costs as they switch from use of heavy fuel oil, or expensive electricity generated from fuel oil, to gas. A cursory glance backwards at the last two decades of Western industrial activity teaches us that even a marginal change in energy costs can cause wild swings in productivity and competitiveness across a developed economy. So one can only begin to imagine what the dramatic shift in energy costs might cause in Israel’s economy, which is already emerging as one of the world’s healthiest and promising. Yet that may not even represent the biggest impact on Israel’s economy. While Israel will continue to be known for its high-tech industry and start-up firms – some of which are energy-intensive industries that might benefit most from lower energy costs – Israel will see a dramatic increase as a result – indirectly or directly – of the emerging gas sector in many tens of billions of dollars’ worth of direct foreign investment and infrastructure projects in the coming decade. When Israel moves from ranking high in small-scale industries, research and development, and start-ups, to mastering large-scale infrastructure as well, it will assume a position in the elite inner circle of the world’s handful of the most advanced economies.

Still, the sudden entry of such a new and important reality into Israel’s economy will also present Israel with considerable economic challenges for which some foresight and strategic planning is in order. Indeed, the Bank of Israel – which was one of the earliest Israeli institutions to grasp the momentousness for Israel of the discoveries – is already engaged in such planning, and its most recent annual report (released April 2013) should be understood in this context. The most important of these long-term dangers is the potential distorting effect of this sector on both Israel’s natural economic advantage of innovation and export, as well as the danger that industries which will enjoy competitively low energy costs may grow to far beyond their sustainable size in Israel, and thus threaten an economic collapse when the gas runs out or increases in price.

The former is generally understood as the “Dutch disease,” namely, that the fortune of great mineral wealth and export eclipses other industries and, even more importantly, drives up the value of the nation’s currency to the point where the nation’s export sector beyond the exported mineral or hydrocarbon resource is no longer internationally competitive. It is for this reason that the Bank of Israel advises against having much of the money gleaned from exports ever enter Israel’s shekel system – and instead prefers to have revenue invested abroad in a sovereign wealth fund. By never entering Israel, never being converted to shekels, nor becoming part of the national budget, the revenue from the resource distorts neither the currency, the economy, nor the nation’s budget process, and thus leaves Israel independent of the eventual downturn when the resource dries up, protects a competitive currency, and leaves its export sector healthy and vibrant.

Still, there is no escaping that cheap gas sold domestically will both deplete the reservoirs rapidly and create entire sectors of the economy whose viability will remain dependent on cheap energy costs. To avoid a situation in a few decades as the resource depletes, when to sustain gas-guzzling industries whose only path to avoid bankruptcy would be massive government subsidies, the Bank of Israel has raised the possibility of imposing consumption taxes on the industrial use of gas to discourage such industries from even emerging.

In short, in terms of economics, with the good will come some challenges, and Israel will need to anticipate and plan carefully to leverage the asset in a way that leaves its economy strong, without allowing vulnerabilities to emerge which in the long run can become devastating strategic vulnerabilities. The bottom line: Israel’s greatest resource is, and must remain, its human capital and industries which tap into it. The nation’s long-term strength depends on the gas’ being leveraged to encourage that, and not to replace or stifle it.

How Gas Affects Geostrategic Conditions

The impact that Israel’s new-found energy abundance will have on its economy and resource scarcity represents a major and positive strategic change in and of itself. If the Tamar field had turned out to be all that was ever discovered, it would have aided Israel through decades of uncertainty until new technologies and means for energy production emerged. It was a bridge to an alternative energy future, but one which represented the first time in Israel’s history that it had energy security.

Yet Tamar was only the beginning. The amount of gas subsequently discovered offshore now dwarfs any feasible, projected Israeli demand for at least half a century. Israel currently consumes about 7 BCM (billion cubic meters) of gas, and is expected to more than double that amount to 15.5 BCM by 2030. But even with these increasing rates of use, the Tamar field’s 275 BCM of gas alone represents two decades of consumption. As such, Israel will become a net exporter of gas, and possibly oil if the latter is discovered later this year.

While the currently known amount of discovered, commercially-producible hydrocarbons do not in themselves make Israel an energy super-major or strategic powerhouse, it is equally true that Israel may have strategic opportunities to leverage the supply of marginally critical amounts of gas to either Europe or Asia. Moreover, precisely because even those marginal additions can have a major impact in key regions, such as Europe, or on the viability of several gas transmission systems, such as those passing through Turkey, Israel’s gas export will carry with it high-stakes geo-strategic plays and competitions, despite its modest size. For example, Israeli gas, while amounting to a small amount if exported to Europe, could represent the marginal difference between tight supply and oversupply, which could cause gas prices to decline, even sharply at times. The decline in gas prices might trample on other nations’ vital interests (not to mention the personal financial interests of their reigning elites) even more profoundly than would losing a few percents of market share. In short, Israel need not export large volumes to attract other nations’ unwanted attention.

Export Destinations in the Region

To Jordan

The easiest, cheapest, and most likely short-term destination for Israel’s natural gas is across the Jordan River to the Hashemite Kingdom of Jordan. When the pipeline from Egypt to Israel was sabotaged twelve times in 2012, each time the gas supply from Egypt to Jordan was also cut, since it went through the same pipelines system. While this pipeline system may not be useful in transmitting Israeli gas to Jordan since it runs through Egypt, connecting Israel’s emerging gas grid to Jordan – especially in the south – is a relatively inexpensive and simple endeavor.

Until Egypt’s gas was cut off, Jordan relied on 2.7 BCM from Egypt for energy production. Jordan had been as much, or even more, dependent on Egypt’s natural gas supply than Israel, having little or no other supply available to compensate. Overall, Jordan imports 97 percent of its fuel needs at a cost of 20 percent of its gross domestic product, and 88 percent of the energy it consumes comes in the form of natural gas. When Egypt’s gas was cut off, Jordan was saddled with extra costs amounting to $5.6 billion for electricity production, forcing the government to increase subsidies by $1.6 billion to avoid doubling the price of electricity.

Jordan is moving to build a major LNG regasification facility in Aqaba on the Red Sea to import gas, but this is still years away and will prove to be very expensive. Moreover, Jordan’s energy despair is a strategic opportunity for others in the neighborhood, especially Iran. Since Jordan represents a critical strategic vortex for wider regional strategic competitions (Syria, Iraq, Palestine-Israel, and even Saudi Arabia in the Hejaz), reinforcing and then addressing Jordan’s dependence in this critical sector becomes a major strategic end in itself for any regional player. Iran, in particular, would want Jordan to become dependent on energy coming from Iraqi areas over which it holds sway – in essence thus exposing Jordan to Tehran’s strategic influence. For Iran, given that Jordan became the home of a mass of Syrian refugees in 2012-13 and is emerging as the gateway for Saudi intrusion into Syria, developing some form of Jordanian dependence on Iran is vital. Controlling the flow of Iraqi gas to Jordan could be the means.

Yet the potential supply of Israeli gas at a rate of 2-3 BCM per annum would completely negate Amman’s vulnerability and stymie Iran’s potential inroad. It appears that talks have already been underway to have Israel’s gas exported to Jordan. Two Israeli papers, Ha’aretz and Globes,7 reported in February 2013 that partners in the Tamar gas field conducted secret talks to deliver gas through the Israeli gas pipeline which supplies gas from Yam Tethys (Mari-B) to Israel Chemicals’ Dead Sea Works plant in Sodom, and then extend the pipeline to reach potash works in Jordan.8 On February 17, 2013, the Jordanian Ministry of Energy and Mineral Resources issued a statement confirming that contacts are currently underway between the Arab Potash Company and its counterpart in Israel through a U.S. company on the possibility of importing natural gas from the Dead Sea area, but denied that there have been direct talks on the issue between the kingdom and Israel on importing natural gas.9

While Jordan will likely become Israel’s first export destination, the amounts will represent only a portion of the total amount Israel will likely export. Israel will almost certainly have much larger amounts to export, and that implies other export destinations in addition to Jordan.

To Europe

The Arab Spring is manifesting itself in subversive acts against major national infrastructure, which in the Arab world is first and foremost the oil and gas pipeline structure. International gas pipelines appear especially vulnerable, as Arab (and even Iranian and Turkish) militaries seem unable to adequately protect them, or perhaps are unwilling to do so.

This upheaval appears foremost to threaten Europe’s energy security. There are five existing or proposed pipelines supplying gas to Europe from North Africa: the Trans-Med pipeline (which carries 30.2 BCM per year via Tunisia and Sicily), the Maghreb-Europe gas pipeline (which carries 12 BCM per year via Gibraltar), the Medgaz pipeline (which flows from Algeria to Almeria in Spain and carries 8 BCM, but is only now about to come on-line), Greenstream (which flows through Western Libya to Sicily and which had carried 11 BCM and is now cut off), and the GALSI pipeline (which is still being planned and will run from eastern Algeria to Europe).

All these pipeline structures originate in the Hassi al-Riml field in Algeria. Thus, three pipelines carry almost 50 BCM to Europe each year, but all originate at one point. Moreover, while the EU sought to diversify its supply of gas by building the Trans-Saharan gas pipeline, which would carry Nigerian gas north, even that pipeline passes through to Hassi al-Riml in Algeria, where it hooks up with the other three currently operating pipelines. Europe’s gas supply – about 18 percent coming through this one point alone (13 percent originating in Algeria and 4.5 percent from Nigeria)10 – is, thus, extremely vulnerable.

This vulnerability has reached near crisis proportions after the “Arab Spring.” As the French intervention in Mali highlighted, the rising tide of Islamist sentiments in North Africa and the Saharan regions threaten the stability of North African states. Centrifugal tendencies have arisen from the breakdown of central authorities in many Arab states and have reinforced the importance of tribe, sect, and families. At the same time, the devastation left in the aftermath of the collapse of the reigning pan-Arab nationalist ideology has driven many to seek the authenticity of Islam. Even without the overlay of ideology, the breakdown of the central state leaves tribes and other local leaders to seek new arrangements with the residual central authority or neighboring tribes or leaders. The presence of an oil or gas pipeline or installation within reach of the tribe – with a choice of either sabotage or protection offered – lends tremendous negotiating leverage. For example, in the first two weeks of March 2013:

- Protestors at the Jalu oil field belonging to Waha Oil in Libya shut down production for over a week, until the Waha Oil company hired local drivers and guards at the field – a demand to which Libya and Waha Oil had to accede.11

- Egypt’s natural gas production continued to decline due to political unrest and tensions. Many drillings in the Nile Delta were stopped due to blocked roads, and several gas and oil fields have been closed under the pressure of local residents. Additionally, Bedouin gunmen in Egypt’s Sinai Peninsula seized and briefly held the country boss of U.S. oil major ExxonMobil and his wife.12

- In Algeria, a movement calling itself “The Committee for the Defense of the Rights of the Unemployed” escalated protests in most southern provinces and prevented by force a meeting of members of parliament in Ghardaia Province. These provinces abut Mali and lawlessness there will likely give a foothold to Malian Tuareg Islamist rebels fleeing French actions to threaten the vital pipeline system.

Even in states which survive, gas transit is not to be taken for granted. For example, to mollify populist sentiment in Morocco, the king has begun speaking about Spanish “occupation” of three slivers of land along the Moroccan coast, including one adjacent to Gibraltar through which the Magreb-Europe gas pipeline passes, which had been under Spanish sovereignty for half a millennium. In early March 2013, Morocco reacted bitterly and lectured the Spanish ambassador to Morocco on a film in Spain about a high-seas collision between a Spanish coastal patrol vessel and a Moroccan refugee ship.13 Behind Morocco’s sudden focus on Spain may lie domestic problems as Morocco faces a rising tide of anti-government protests.

Moreover, we already see in both Algeria and Libya how the energy sectors there are rapidly becoming the victims of labor unrest and stoppages,14 and how tensions in Mauritania can affect transmission systems to Morocco, as various groups begin to understand how to leverage the sensitivity of that sector for their uses. While labor unrest or stoppages are not new, the climate in North Africa is so explosive that unrest in such places as Algeria, Morocco, or Libya could escalate from a seemingly contained local issue to a national breakdown of order in just days.

Thus, countries along Europe’s southern littoral are rethinking their dependence and diversification strategy, at the same time that they also seek to reduce dependence on Russia, block shale-gas development, and cut back on nuclear power.

In short, anchoring more than a sixth of Europe’s entire gas supply to an area being torn apart by collapsing states and tempted by Islamic ideology is the new reality which European energy planners must face. Europe’s grim reality could represent a unique window of opportunity for Israel to nail down long-term agreements and align export policy with a broader effort to reset Israeli-European relations.

At the same time, as noted, any Israeli gas trade with Europe is not without complications and risks. It will inherently cross Russia’s domination of Europe’s gas supply. Israel’s gas offers a backstop against Russian threats to cut off supply as blackmail – much as Moscow has done in the past with gas pipelines to Ukraine – but that is not the primary strategic challenge to Russia which Israeli gas could pose. A marginal addition of gas supply to Europe, such as what Israeli imports could represent, can create mild oversupply. But even mild oversupply can cause prices to drop sharply in the European region – which whittles down the bottom line of Russian gas companies integrally linked to Russia’s ruling elite.

Only too aware of the threat of eastern Mediterranean supply if Europe is able to diversify away from Russian gas dependency, Moscow is constantly attempting to buy long-term into the Israeli gas and oil energy bonanza. On February 26, 2013, Russia’s Gazprom clinched a key deal to market Israeli liquefied natural gas (LNG) from the Tamar offshore field for 20 years. Gazprom is also eyeing a role in the development of Israel’s gigantic Leviathan gas field.15 Still, the Minister of Energy and Water Resources moved quickly to remind the Tamar partners that such a deal requires approval of his ministry, and that the Tamar field is largely to be designated for domestic consumption. In essence, he nixed the deal. Thus, Russia’s attempt to enter remains unsatisfied, though closer than ever.

It is possible that selling gas to Europe may not offer the leverage for which Israel would hope. Europe already is increasingly dependent on Israeli high-tech in critical sectors of its economy. Yet such dependence has done little to alter what Israel views a continued European drift toward greater antagonism toward Israel. Perhaps this might fundamentally shift were the amount of hydrocarbon resources to emerge in Israel so large as to begin to replace, and not only compete with, Russian gas and Arab oil. But that potential has still to be realized. As things now stand, there are some economic opportunities to sell gas to Europe, but there are also great advantages to having Israel sow more fertile ground and use the export of natural gas to enhance its relations with friendly Asian powers, and possibly even with China.

To Asia

Asia may emerge as Israel’s preferred export destination. While the prices that the Leviathan partners could govern by trading with Asia are higher, the price is only partially the reason why Asia will likely emerge as an export destination. The partnership currently owning Leviathan is generally assumed to lack the means to bring this complex, challenging, and very expensive project from ground to market. As such, the partners have already signed an initial agreement with the Australian firm, Woodside, to acquire about a third of the rights to the field in order to tap into its liquefaction experience, marketing structure, and capital. But Woodside is oriented toward marketing gas in Asia, and has structured the initial agreement to a schedule for building a liquefaction plant generally assumed to service trade to Asia. In short, the shape of the partnership will have a significant impact on whether the gas flows east or west.

While the export destination of Israel’s gas – namely east to Asia or west to Europe – is strategically important, the context and geostrategic circumstances of how and through what the gas will be transmitted to either Europe or Asia must first be examined, since these latter factors may dictate the shape of the former.

Export Transmission Structures

Selling natural gas to either the European or Far Eastern markets presents both geo-strategic opportunities and challenges. But getting the gas from Israel and Cyprus to those markets will also necessitate complex transmission infrastructures, which themselves affect and are affected by geo-strategic conditions.

Uniqueness and Rigidity of Gas Infrastructure

Unlike oil, gas neither flows to spot markets nor is sold en route to a consumer. There is no global market price, like Brent Sweet Crude for oil. Gas is priced uniquely to each deal and priced more by nation or region. It is not globally traded as a commodity. The infrastructure to transmit gas – either via pipelines or liquefaction – is so complex, demanding, and expensive that marketing agreements and supply patterns are locked in for the long term, indeed years before the gas even flows. Even liquefied gas shipped from port to port is essentially a “locked” structure much like train lines.

The country supplying and the country receiving the gas, therefore, tether their critical energy policies on the expectation of a particular supply chain, and are thus tied to a particular diplomatic relationship for years. The severing of a particular source of gas supply is not easily replaced in ad hoc fashion by oversupply from elsewhere; it is strategically important for a nation even when it only represents a relatively small portion of its overall supply. Thus, even modest amounts of Israeli gas exports can carry significant strategic leverage. Yet the inverse is also true: a consumer also cannot be easily replaced. Thus, the gas trade carries strategic importance and leverage for both the supplier and consumer, especially when the provider is exporting to only a few consumers. The greater the amount of gas Israel discovers, therefore, the greater it inoculates itself from dependence on the consumer.

The short-term inflexibility of the gas trade, and the difficulty of replacing disrupted supply, implies as well that prices for energy for consumers and revenues for suppliers can be easily manipulated by marginal increases or decreases in supply. This price sensitivity, which can translate to substantially fluctuating costs for consumers or revenues for suppliers, therefore makes the question of gas supply strategically vulnerable to the geopolitical interests and machinations of third parties. As such, two factors – the strategic context of gas transmission structures and third-party strategic ambitions – are often as important to understanding the overall strategic significance of a specific gas-supply relationship as the two-dimensional question of supply and consumption for the two nations’ involved in the trade themselves.

Via Jordan

There are voices in the Israeli government, and more across Israel’s political spectrum, who view the anchoring of an export structure to a liquefaction terminal in Aqaba, Jordan, on the Red Sea – as an important strategic objective. Moreover, there is a powerful constituency, reinforced by international diplomatic preferences, to advance the option of lashing Israel and Jordan tightly together through natural gas structures as a way to advance the peace process.

Still, it is highly unlikely that this option will ultimately prevail. Israel’s recent experience with Egypt, where half of Israel’s natural gas supply was permanently severed because of the destruction of the Egyptian-Israeli gas pipeline following the collapse of the Mubarak regime, suggests that Israel will view with apprehension any scheme to anchor its critical infrastructure and an emerging major portion of its GDP to a potentially unstable Jordanian regime.

Even assuming the Jordanian government does survive, political conflict in the Middle East in the age of the Arab Spring is increasingly expressing itself through attacks on energy infrastructure, particularly pipelines. Since Iran, Syria, and Hizbullah already have defined Israel’s gas industry as a strategic target, Israel’s government expects them to attempt to strike Israel’s export structure at any point of vulnerability. Moreover, Iran and Turkey, which have had some role in the attacks on each others’ pipelines in Iraq, Syria, and Turkey, both view the successful emergence of Aqaba, Jordan, as a major energy transfer hub with tremendous strategic apprehension. In order to vie for control and undermine the viability of an emerging Kurdish state, both want all northern Iraqi gas and oil – such as what is in the area around Taktuk, near Chamchamal in the Buvanoz region – to either remain undeveloped or flow through their respective territories, and will thus seek to sabotage any alternative, such as Aqaba:

- Iran wants to control the trade of Iraqi gas. First, it needs gas for its Azeri provinces. Currently, there is no national gas net transporting Iran’s enormous gas reserves in South Pars in the Gulf to its populations along the Caspian Sea who suffer almost chronic natural gas shortages. Inasmuch as gas flows to Europe from Iraq, Iran wants it to flow via the pipeline system it is planning through northern Iraq to Syria, bypassing Turkey which it cannot trust. For Asia, Iran wants the gas to reach the sea via its planned pipeline system to the Persian Gulf and Indian Ocean.

- Turkey has an almost parallel outlook. First, it wants Iraqi gas in order to address its own gas shortages, which are increasing to critical levels. Second, Turkey is moving to become the exclusive conduit for all oil and gas from the Kurdish areas to Europe. It wants Iraqi gas flowing to Europe to be dependent on its emerging pipeline system, such as the Kirkuk-Yormortluk pipeline, which has three parallel pipes carrying gas (1) and oil (2), and ultimately connecting to the EGE Gaz LNG plant in Aliaga (about 35 miles north of Izmir along the Aegean seacoast). This pipeline is already hooked up to the Turkish system and sits at the Turkish head of the Trans-Aegean Pipeline (TAP). Turkey views the TAP as a bottleneck structure: both Nabucco and the planned EGL gas pipelines will run through the TAP, and thus would want to have Iraqi gas flow through it rather than bypass it. Third, Turkey would want gas flowing to Asia from Iraq to pass through its pipelines, be liquefied at the EGE Gaz plant in Aliaga, and loaded onto ships going to Asia via the Suez Canal.

As such, Jordan’s participation in any gas transmission structure other than a limited one to import Israeli gas will only load onto Amman an even greater strategic headache atop one already reaching unmanageable proportions.

Via Cyprus

Early discussions after the Leviathan field was discovered focused on building a pipeline from Israeli fields, through Cyprus, to Greece. Notably, from the time Leviathan was announced to early fall 2011, there was almost no discussion about placing an LNG terminal in Israel. Most inside the Israeli government focused on placing it either in Cyprus or Jordan, largely under the assumption that any LNG project outside Israel would encounter fewer geopolitical problems and enjoy a vastly simpler zoning/permitting process.

Significant voices within Israel’s foreign policy establishment, most notably in the Foreign Ministry (which includes some diplomats on assignment in key positions to other ministries such as the Ministry of National Infrastructures), also signaled that they want to align Israel’s export structure with its emerging relationship with Cyprus and Greece.

But the tide later shifted. While Israel’s Foreign Ministry, as well as apparently some companies involved,16 still entertain the idea of placing the LNG infrastructure in Cyprus, tensions over Cyprus, the growing role that Gazprom and Russia appear to be playing there, and the overall instability and potential corruption which appears to be plaguing Cypriot politics and business appear to have reminded many in Israel’s government that, from Israel’s geostrategic perspective, placing critical infrastructure in Cyprus is problematic.

Moreover, the attractiveness of Cyprus diminished within the context of change in Egypt and the entry of the Australian firm, Woodside, as an equal partner in the Leviathan field. Any eastward-directed export infrastructure anchored to Cyprus would tend to rely strongly on free and safe passage for Israeli gas shipments through the Suez Canal. In essence, this locks what will emerge as Israel’s most vital industry into a trade route that passes through an Egypt politically dominated by the Muslim Brotherhood, which remains ideologically opposed to provisions in the 1979 peace treaty allowing Israeli passage through the Canal.

Finally, although since the mid-1970s Cyprus has enjoyed a record of stability, several key trends indicate instability likely will rise in Cyprus in the coming decade.

Turkish Prime Minister Erdogan’s convictions and desire to reestablish a neo-Ottoman imperial empire under a rehabilitated “Caliphate” has driven Turkey to regard the Greek islands, the Balkans and Cyprus, as well as Syria, Iraq, Lebanon and Israel-Palestine, as “lost territories.” After a year of increasing tensions between Turkey, Greece and Cyprus, in May 2012, the Turkish Foreign Ministry issued a press release, in response to Cyprus’ issuing of international tenders for off-shore hydrocarbon licenses, saying that Turkey will give every support to the Turkish part of north Cyprus (TRNC) by “acting upon its responsibilities as a motherland and a guarantor power.”17 The term “guarantor power” refers to the “Treaty of Guarantee” which was signed in 1960 by the Republic of Cyprus, Greece, Turkey and the UK, and following which Cyprus became independent. That treaty made Greece, Turkey and the UK guarantors of the independence, territorial integrity and security of Cyprus. Article 4 of the treaty permits the guarantors to take action, even unilaterally, in order to reestablish the state of affairs created by the treaty, and Turkey used it when it invaded Cyprus in July 1974 in reaction to the coup d’etat which the Greek junta carried out in Cyprus in order to unite it with Greece. Turkey thus signaled that in reaction to what can be construed as a change of the status quo, it might take action, and this could include the use of force.

The symbolism of how Turkey names its gas and oil exploration ships reinforces the alarm these statements should cause. Turkey’s 3D seismic study vessel Polarcus Samur was renamed the Barbarossa Hayreddin Pasha. Barbarossa Hayreddin Pasha was the Ottoman admiral whose naval victories secured Ottoman dominance over the Mediterranean during the mid-sixteenth century. In 2011, Turkey renamed the first of its exploration ships the Piri Reis after a famous Ottoman geographer and cartographer who was also the commander of the Ottoman fleets in the Indian Ocean and in Egypt. Among his feats were the recapture of Aden and Muscat (in 1548 and 1552, respectively) from the Portuguese and the subsequent capture of the strategic island of Hormuz, of Qatar and of Bahrain. The naming of these two ships symbolically connects Turkey’s present push in the eastern Mediterranean with Ottoman imperial exploits in the Middle East.

The shift in Turkish rhetoric and symbolism on Cyprus should be seen in the context of a deeper strategic movement which makes it unlikely that Cyprus will continue to enjoy the same strategic stability it has had for the last four decades.

- While never having surrendered its claims in Cyprus, the island’s apparent stability since the mid-1970s has been linked to Turkey’s attempt to enter the European state system. The more Turkey reorients and aspires to assert its Middle Eastern and Islamic aspects, the more its claims in Cyprus assume importance and intensity.

- Turkey’s Islamist government under the AKP believes the military anchors the Turkish state to the West. Rending the relationship between Turkey and the West weakens the stature of the military internally. As such, the AKP seeks wedge issues to force the military to choose between its relationship with the West and its need to embody nationalist sentiments. Cyprus is such an issue. Thus, Turkey’s continued presence in NATO no longer deters Ankara from acting, since it may be precisely that relationship which Erdogan may want to sever by provoking a confrontation.

There are also signs that Cyprus’ strategic challenges may grow in the future as Egypt and Turkey draw nearer, bound by a common Islamist sentiment. Indeed, the Legislative Committee of Egypt’s upper house approved a draft law in March 2013 canceling the agreement on maritime borders between Egypt and Cyprus and calling for the creation of new borders surrounding the economic zone in the presence of Turkey as a third party.18 The proposed law was submitted by MP Khaled Abdel Qader Ouda, who said that the agreement signed by Cyprus and Israel last year invalidated the Egyptian-Cypriot deal of 2003, since Egypt had the right to be present at the signing. Cyprus played down these reports since Egypt’s executive branch has not questioned the agreement between two signatories of the Convention on the Law of the Sea, which has been submitted to the UN, and said: “Cooperation in the field of hydrocarbons’ development in the areas adjacent to the Median Line of the EEZs of the two countries, as well as cooperation in other related fields, ranks high in relations and dialogue between governments.”19

That said, it is warning shot across the bow – the Islamization of Egypt is likely to unsettle Cyprus’ relations over the long term to the south, and encourage its northern nemesis to be more aggressive in cooperation with Cairo. Indeed, Cypriot papers have reported that Turkey has been leaning on both Lebanon and Egypt to reject the EEZ agreements signed with Cyprus.20

Even beyond the Turkish and Egyptian questions, there are worrisome security aspects to Cyprus. Hizbullah, Syria and Iran in no way want to see the Levant basin’s assets be developed. But their ability to stop Israel from developing its natural gas discoveries is very limited. Indeed, Israel has successfully protected its vital infrastructure even in periods of all-out war. But Cyprus is not secure from international terror, and Hizbullah, Iran, Syria, and secular Palestinian groups under Syrian control all have a strong operational presence in Cyprus, and could potentially find ways to strike at a joint Cypriot-Israeli LNG facility. Cyprus is simply not as able as Israel to develop the means to protect it.

Finally, there is the complex role of Russia regarding Cyprus. A review of Russian offers to “help” Cyprus over the last two years suggests less altruism and more strategic interests.

- Cyprus, which is already a leading offshore center for Russian capital and finance, on October 5, 2011, announced it would get a 2.5 billion euro loan from Russia at an interest rate of 4.5 percent.21

- Russia was the first and strongest supporter of Cyprus’ position in the gas exploration escalation with Turkey in summer 2011,22 and moved its fleet into the eastern Mediterranean23 (specifically, the Russian aircraft carrier Admiral Kuznetsov and a submarine for “patrol purposes”) to deter Turkey from acting.24

- In January 2013, Russia’s state-run gas monopoly Gazprom offered just under 2 billion euros for DEPA, Greece’s state owned gas company. DEPA supplies gas to major consumers in the country, and 65 percent of its shares belong to the Greek government. Despite the fact that this sum is much higher than DEPA’s real value, this deal helps Gazprom strengthen its monopoly on the Greek energy market and its position in Europe. Indeed, Russian analysts have noted that after buying DEPA and after the launching of the South Stream gas pipeline in the future, Greece, Bulgaria, Serbia, and Croatia will all come under the control of Gazprom as a supplier of gas.25

- On March 17, 2013, in reaction to Cyprus’ plan to tax bank deposits to address its financial crisis, Gazprom submitted a proposal to the office of Cypriot President Nicos Anastasiades to undertake the restructuring of the country’s banks in exchange for exploration rights for natural gas in Cyprus’ exclusive economic zone and substantial control over the country’s gas resources.26

- Cypriot President Anstasiades was unwilling to discuss Russia’s offer, but Russian officials (responding via the Association of Regional Banks of Russia) said: “Now the faith in Cyprus as a place where it is convenient to keep one’s money will be undermined” and that Cyprus’ banking system is “not trustworthy” and advised Russian citizens “to withdraw their deposits from Cyprus.”27

Given the strategic centrality of gas to Israel’s emerging strategic position, and the strong interests of Turkey, Iran, and others to challenge it, it is important that Israel’s key infrastructure fall under the umbrella of Israeli power. Since Israel cannot project its military capabilities to “own” the strategic defense of Cyprus – or even to guarantee security on the ground for key Israeli interests – it would make sense for Israel to keep its vital natural gas infrastructure in Israel itself and not anchor it to a Cypriot LNG structure.

Indeed, it might even make sense to anchor the emerging Cypriot gas industry on an Israeli distribution structure, rather than vice versa, since it would anchor the strategic interests of both Greece and Cyprus, and even the EU, to the defense of Israel to ensure that the Levant basin production is protected. It may be a stretch to convince Europe that its vital interests and the safety of natural gas coming from the eastern Mediterranean are better guaranteed by building a key piece of its gas infrastructure in Israel, but when the overall direction of the region is taken into account, and the very real possibility that the equilibrium in Cyprus can unravel is considered, it becomes far less of a stretch.

Via Turkey

Most recently, the idea surfaced that Israel could build an export pipeline from the Leviathan field to Turkey.28 At the end of January 2013, the director-general of Israel’s Ministry of Energy and Water Resources, Shaul Tzemach, indicated that Turkey could be an anchor customer for Israeli gas, and that the option of gas exports to Turkey was practical, despite political tensions. Talking about cooperating with Turkey, he said, “This isn’t out of the question. There are quite a few geopolitical barriers, but if we know how to create the right conditions, it is possible. Gas should be used as a stabilizing factor which leads to cooperation between countries and includes multinationals and international parties with an interest in regional stability.”29 Tzemach added that there is room to include foreign powers and multinationals in a project which would export Israeli gas to Turkey. According to another Israeli financial paper, Turkish conglomerate Zorlu Endustriyal ve Enerji Tesisleri Insaat Tie AT would be the Turkish partner in an Israel-Turkey gas pipeline.

While officials from Turkey appear less eager, their actions and warnings continue to suggest the Turkish option is at best questionable. Almost the same day Tzemach was quoted, Turkey’s deputy energy minister, Murat Mercan, was berating an Israeli diplomat in a public forum and laid out an extremely tough position, saying that even if Israel fulfilled Turkish demands for 1) an open apology for the Mavi Marmara incident, 2) compensation for families of the victims, and 3) ended the blockade on Gaza, Israel’s resource cooperation with Greek Cyprus would preclude any energy cooperation with Turkey.30 While the first of these seems to have been satisfied, it is not yet clear at this writing whether the other conditions will be resolved to Ankara’s satisfaction.

Turkey may not be prepared to compromise on energy cooperation with Cyprus, which it views as a red line. Turkey announced on March 27 that the government wants to suspend some of Turkey’s projects with Eni, the Italian oil and natural gas giant. Turkey’s Energy Minister Taner Yildiz said, “We decided not to work with Eni in Turkey, including shelving their projects,” because of Eni’s plans to explore offshore of Cyprus, which Turkey claims are in violation of international law. Yildiz also said the Turkish government would prefer that Istanbul-based Calik Holding did not work with Eni on a project to build a 550-kilometer crude oil pipeline to connect the Black Sea port of Samsun with the Mediterranean port of Ceyhan. Turkey’s move also conveys high-stakes strategic signaling. Eni was working with Russia’s Gazprom to build the South Stream pipeline to carry Russian gas through Turkey. Turkey was signaling Russia, and not only Italy and Eni, that if they develop their ties with Cyprus, they will lose their role in the strategically important South Stream project, which could then compete with Russian gas firms rather than service them.

Moreover, despite apologies and an air of détente, the long-term trends indicate that broader tensions between Israel and Turkey will continue to grow rather than recede because of the ideological outlook governing Ankara as it seeks to rehabilitate its bygone Ottoman glory.

From the standpoint of Turkish-Israeli relations, even if such a pipeline were built, it would be subject to:

- Geopolitical blackmail on Ankara’s part: In the era before Israel’s gas discoveries, Turkey’s government nixed the idea of building a water pipeline to Israel until Israel gave in on all issues with respect to the Palestinians.

- Vulnerability to sabotage: Pipelines to Turkey are bombed regularly. Pro-Turkish saboteurs have regularly been blowing up pipelines carrying oil from northern Iraq to Syria in an effort to destabilize the Syrian government – a nearly monthly occurrence. In response, pipelines supplying gas to Turkey from northern Iraq and even Iran have been bombed regularly. Indeed, it is the tenuousness of pipeline supply to Turkey which has led to the Turkish government’s interest in the Israeli pipeline, which it will be no more able to secure than its other pipelines.

- Geostrategic opposition from Moscow: Israeli gas poses a competitive pressure on Russia’s supply to Turkish and European gas markets. It may be possible to address this concern by bringing Gazprom into the deal in a controlling position, but bringing in Gazprom would only multiply the geopolitical vulnerability to blackmail and expose the pipeline system to Turkish-Russian and Russian-Israeli issues in addition to Turkish-Israeli ones.

But even more important is that Russia now sees itself threatened by the rise of a resurgent Ottoman Sunni empire to its south and is seeking every way possible to cut Ankara’s ambitions down to size. It would be a risky endeavor to be on the wrong side of Russia and Iran on the issue of a facility in Turkey which cannot be effectively protected from terror.

Export Direct from Israel to Markets

Thus, it is likely that ultimately the gas will be liquefied on Israeli territory and exported directly via sea to the consuming market. Indeed, the Tzemach Committee – the Israeli governmental committee tasked with setting Israel’s overall natural gas policy – expressed a “strong preference” that any export facility be located on Israeli territory. In addition, officials from Israel’s Ministry of Energy and Water Resources have told the Israeli press that the terminal should be built in Israel, despite the bureaucratic difficulties, since “no sensible government is prepared to have its gas export installations in another country, however friendly it may be.”31

Israel’s government may also seek to leverage and align gas export policy to broader foreign policy objectives by favoring a flexible export strategy that exploits the country’s geographic position to service both Asia and Europe. Israel and Egypt have the geographic advantage of relatively ready access to both Asia and Europe, therein allowing both to contemplate a dual-continent approach to export. Adopting such a plan potentially could involve the construction of LNG terminals anchored at either end of the Eilat-Ashkelon Pipeline Corp. (EAPC) structure – with terminals in Ashkelon on the Mediterranean facing Europe and in Ramat Yotam near Eilat facing Asia – depending on the volume of resources discovered in the Levant Basin.

Indeed, many Israeli officials view the importance of gas export in the context of Egypt’s deterioration – not only in terms of hostility to Israel, but in terms of anti-Western tendencies and chaos, all of which raise questions about the viability of the Suez canal as a major European-Asian transit route. These officials see a cross-Israel natural gas pipeline as an additional anchor for transforming Israel into a major trans-ocean passage way connecting the Mediterranean and Red Seas and reasserting the Land of Israel as a major trade and transport route as an alternative to Suez. They view the development of the Eilat area, and Israel by extension, as Europe’s portal to Asia, thus enhancing the strategic value of Israel to the West.

Rising Iranian Naval Threats to the Red Sea

But even an export structure operating directly from Eilat (Ramat Yotam) to markets in Asia would face a rising strategic problem which could drive a fundamental shift in Israel’s naval posture and doctrine: Iran’s increasing naval presence in the Red Sea.

- On January 28, 2013, Iran’s foreign minister noted that Iran attaches “grave importance” to the security of the Red Sea, and that its naval presence in the Red Sea is a significant step towards building good relations with the regional states.

- On January 16, 2013, Iran Navy Commander Rear Admiral Habibollah Sayyari said that the Islamic Republic’s 24th fleet of warships will be deployed to the Mediterranean Sea. “The Navy’s 24th fleet of warships will patrol the north of the Indian Ocean, the Gulf of Aden, Bab-el-Mandeb, the Red Sea, Suez Canal and the Mediterranean Sea for three months and will even sail as far as southeastern Asian countries,” as part of the Velayat 91 exercises.32

- On December 28, 2012, Iran announced that its 23rd fleet, with two warships, docked in Port Sudan on December 8, after patrolling the strategic Bab el-Mandeb Strait and the Red Sea. The Navy said that the 23rd fleet comprised the Jamaran destroyer and the Bushehr logistical vessel. Sudan’s top navy commander Abddulla al-Matri at the time called for the further expansion of military ties between Iran and Sudan.33

- The two naval visits by Iran prompted a Sudanese opposition news website to report on December 9 that the Iranian Revolutionary Guards and Sudan agreed to establish an Iranian military base on the Sudanese Red Sea shore and the repeated visits to Sudan by Iranian naval units are intended to prepare international and Sudanese public opinion and gauge reactions toward the establishment of the military base.34

- An Iranian state-owned media network reported that the 22nd fleet, comprising a helicopter carrier and a warship, which were deployed to the coasts of Djibouti and Bab el-Mandeb Strait in late September, visited Sudan on October 29 as part of a 75-day mission.35

Israel’s Navy Will Come of Age

Israel will likely send the bulk of any gas it exports eastward. The new gas trade, however, will echo the shift already underway in Israel’s export patterns more broadly as Israel’s economy increases trade with Asia, while decreasing trade with Europe. This new energy trade and expanding non-hydrocarbon exports to Asia will coincide with and reinforce Israel’s broader plan to offer a strategic alternative to Suez Canal transit.

This expanding role of positioning Israel as the gateway to Asia from Europe will involve strategic challenges that will encourage Israel not only to reinforce its naval cooperation with the U.S. (and perhaps some European navies as well). It will also require Israel to establish and expand a Red Sea fleet with a blue water capability and significant convoy capabilities. This will become all the more important as U.S. naval power recedes globally over the next decade.

At the same time, the significant destabilizing forces at work in the eastern Mediterranean – where the production fields are actually located – and the decreasing role of the U.S. navy in securing the area will create a void and danger to Israel’s offshore assets there. This, too, will demand a significant expansion in the size and capability of Israel’s Mediterranean fleet.

In short, Israel’s navy will become one of the Israel Defense Force’s most important arms to secure the natural gas and potentially oil trade which will change Israel in the coming decades.

Considerations for the Future

While self-sufficiency in energy – and by extension in water resources and in economic vitality – which Israel’s discoveries allow will represent a substantial improvement in its strategic strength, eventual export of its hydrocarbon resources will involve far more weighty and complex considerations. Yet, even at this early date, several key themes emerge.

Attempts to employ these resources for the sake of advancing peace between Israel and its Muslim neighbors will be the greatest temptation at the policy level. Yet the historical record suggests that increasing co-dependency between Israel and its neighbors and using development efforts to anchor rapprochement among populations are quixotic cul-de-sacs. Such efforts in the past only increased Islamic resentment against Israel and played into their ideologues’ anti-Semitic imagery of Jewish control of their economies. Furthermore, they have left Israel more strategically vulnerable. While some in Israel hope that anchoring Israel’s export system to Turkey and becoming an answer to Turkey’s energy gap will help reverse the strategic foundering of the bilateral relationship, Israel’s experience with Egypt and the Palestinians suggests that such hopes, while well-intended, will meet with great disappointment.

The introduction of any additional party to Israel’s export system will add – likely geometrically – to the strategic complexity and difficulty of realizing and maintaining that structure. While at first glance Cyprus and Jordan may appear to be elegant solutions to the difficulties and dangers of emplacing major facilities in Israel, the emerging instability of these two countries, as well as their indigenous military weakness and darkening strategic positions, will be far more threatening than the situation in Israel in the coming decades. They are both far more vulnerable and far less capable of managing the shifting strategic realities of the Middle East and eastern Mediterranean than Israel. In short, Israel’s export structure should be as direct, bilateral, and independent as possible. The temptation to encumber it with regional hopes and diplomatic missions should be resisted, no matter how promising they appear.

The strategic challenges posed by the near- and medium-term decline of U.S. power, the changing regional order, and Israel’s rising resource importance will further combine to demand of Israel a significant doctrinal shift in its military posture and a substantial increase in its military spending.

* * *

1. The Marker, Ha’aretz, January 9, 2011.

2. Sharon Kidmi, “BG: No chance we will ever do business again in Israel,” The Marker, May 21, 2006.

3. Amiram Barkat, “Where are the oil majors?: Unlike neighbor Cyprus, Israel has failed to attract top league companies to its burgeoning energy industry. Why?” Globes, June 4, 2012.

4. According to Israel’s Natural Gas Authority of the Ministry of Energy and Water Resources.

5. http://www.globes.co.il/serveen/globes/docview.asp?did=1000829662&fid=1725, March 13, 2013; http://www.themarker.com/dynamo/1.1963777, March 13, 2013.

6. Remarks (Altman) in interview conducted May 17, 2010, in Washington, D.C.

7. http://www.globes.co.il/news/article.aspx?did=1000823101#fromelement=hp_firstarticle, February 18, 2013.

8. http://www.haaretz.com/business/jordan-in-secret-talks-to-import-natural-gas-from-israel-s-tamar-field.premium-1.503672, February 15, 2013.

9. http://jordantimes.com/arab-potash-company-looks-to-import-natural-gas-from-israel, February 17, 2013.

10. European Commission, EuroStats, http://epp.eurostat.ec.europa.eu/statistics_explained/index.php/Natural_gas_consumption_statistics#Supply_structure

11. Al-Jazeera, March 17, 2013.

12. Regarding declining production rates, see http://www1.youm7.com/News.asp?NewsID=975119&SecID=24&IssueID=0, March 11, 2013. About Bedouin kidnapping of Exxon executive, see http://www.reuters.com/article/2013/03/07/us-egypt-kidnapping-idUSBRE9260YW20130307, March 7, 2013.

13. “Tension mounts between Morocco, Spain over boats collision,” Moroccan MAP News Agency, March 13, 2013.

14. Tout sur l’Algerie website, March 30, 2013.

15. Peter C. Glover and Michael J. Economides, “Russia’s New Middle East Energy Game,” Commentator, March 2013, http://www.thecommentator.com/article/3048/russia_s_new_middle_east_energy_game

16. http://www.cyprusnewsreport.com/?q=node/4842, November 2, 2011 and http://famagusta-gazette.com/noble-energy-manager-expresses-hopes-for-giant-gas-fields-in-cyprus-p13390-69.htm, November 2, 2011.

17. http://www.mfa.gov.tr/no_-140_-18-may-2012_-press-release-regarding-the-international-tender-for-off_shore-hydrocarbon-exploration-and-exploitation-opened-by-the-greek-cypriot-administration.en.mfa, May 18, 2012.

18. Quoted by http://www.egyptindependent.com/news/shura-council-approves-draft-law-cancelling-egypt-cyprus-economic-zone, March 6, 2013.

19. http://famagusta-gazette.com/egypt-has-never-questioned-the-eez-agreement-with-cyprus-fm-stresses-p18446-69.htm, March 7, 2013; http://www.cyprus-mail.com/cyprus/minister-plays-down-egypt-pulling-out-eez-reports/20130308, March 8, 2013.

20. http://www.cyprus-mail.com/cyprus/minister-plays-down-egypt-pulling-out-eez-reports/20130308, March 8, 2013.

21. http://www.financialmirror.com/news-details.php?nid=24628, October 6, 2011.

22. http://www.cyprus-mail.com/cyprus/greece-and-russia-rally-behind-cyprus/20111002, October 2, 2011.

23. http://famagusta-gazette.com/minister-violations-of-cyprus-air-space-by-the-turks-is-an-everyday-pheno-p13115-69.htm, October 4, 2011.

24. http://www.asianews.it/news-en/Turkey,-Israel,-Greece-and-Russia-mobilising-over-Cyprus-gas-22820.html, October 5, 2011.